Own a Share in Premium Residential & Commercial Properties Starting from Just ₹15 Lakhs. Secure, Profitable, and Accessible Investments Await!

RBI’s New P2P Lending Guidelines: How They Impact Platforms, Lenders, and Borrowers

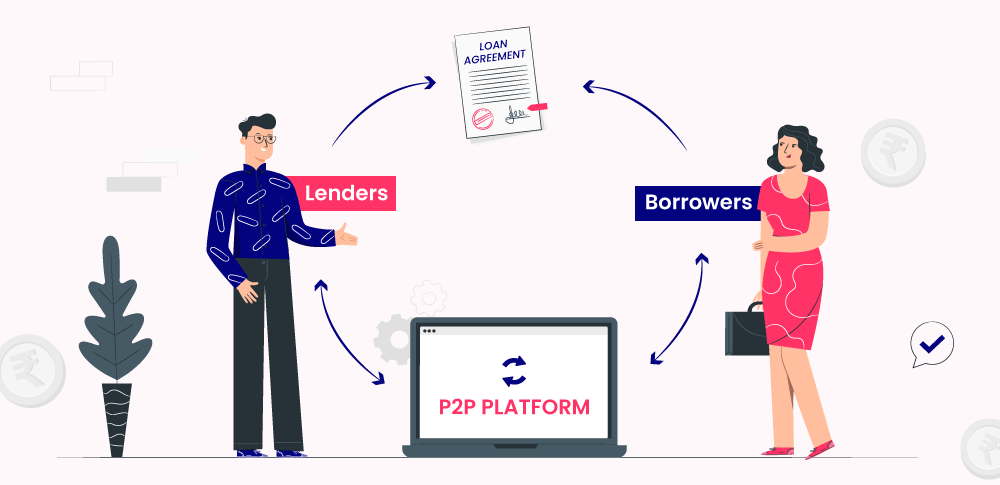

Peer-to-peer (P2P) lending has become a popular alternative to traditional banking in India, providing a platform for individuals to lend and borrow money directly without the intervention of banks. In this blog, we’ll explore the latest RBI guidelines for P2P lending platforms and discuss their impact on platforms, lenders, and borrowers.

8/28/20243 min read

Overview of RBI’s Revised P2P Lending Guidelines

The RBI’s updated guidelines aim to refine the operational framework of Non-Banking Financial Company-Peer to Peer Lending Platforms (NBFC-P2P). These revisions focus on curbing risky practices, enhancing transparency, and safeguarding the interests of all parties involved. Key changes include banning credit guarantees, enforcing stricter fund transfer rules, and mandating monthly disclosures of platform performance. Let’s dive deeper into these changes and their implications.

Key Changes in P2P Lending Regulations

1. Prohibition of Credit Guarantees by NBFC-P2P Entities

The new guidelines prohibit NBFC-P2P platforms from providing credit guarantees or enhancements, which previously assured lenders of returns even in case of defaults. This rule ensures that lenders understand the inherent risks of P2P lending, as the responsibility for credit risk now rests solely on them.

Impact:

For Lenders: Increased risk awareness; potential for higher returns due to a true assessment of borrower creditworthiness.

For Borrowers: Likely to face slightly higher interest rates as lenders adjust for unguaranteed risk.

2. Fund Transfer Through Escrow Account: T+1 Rule

The RBI now mandates that funds in escrow accounts be transferred within one business day (T+1) of receipt, enhancing the speed and efficiency of transactions.

Impact:

For Lenders: Faster access to repaid funds.

For Borrowers: Quicker disbursement of loans, which is critical in emergencies.

Industry Response: Platforms are requesting an extension of this timeline to T+2 or T+3, citing operational challenges.

3. Cap on Lending Amounts and Net Worth Requirements

The cumulative lending cap for individual lenders across all P2P platforms is now set at ₹50 lakh. Those wishing to lend more than ₹10 lakh must provide a net worth certificate, ensuring that they have sufficient financial backing.

Impact:

For Lenders: Protects against over-leveraging and potential financial distress.

For Platforms: Promotes broader participation by preventing risk concentration.

4. Restrictions on Cross-Selling of Products

P2P platforms can no longer cross-sell products other than loan-specific insurance, aimed at reducing conflicts of interest and ensuring that borrowers are not overwhelmed by unnecessary add-ons.

Impact:

For Borrowers: Simplifies borrowing decisions without the pressure of additional products.

For Platforms: Refocuses operations on core lending activities, potentially lowering compliance complexities.

5. Monthly Portfolio Performance and NPA Disclosures

To promote transparency, platforms must now provide monthly disclosures of portfolio performance, including data on non-performing assets (NPAs).

Impact:

For Lenders: Empowers informed decision-making with access to up-to-date platform performance data.

For Borrowers: Could lead to more competitive rates as lenders refine their risk models based on disclosed data.

6. Revised Fee Structures

The RBI now mandates that fees charged by P2P platforms be either fixed amounts or percentages of the principal loan amount, eliminating performance-contingent fees.

Impact:

For Lenders and Borrowers: Greater clarity on costs, enhancing trust and predictability in the lending process.

For Platforms: Aligns revenue generation with facilitation services rather than loan performance.

Industry Reactions to the Revised Guidelines

P2P platforms have voiced concerns, particularly about the T+1 settlement rule. The Association of P2P Lending Platforms plans to approach the RBI for an extension, arguing that the stringent timeline could pose operational challenges. However, the RBI’s primary intent remains clear: to protect lenders’ funds by ensuring timely transfers.

Current Landscape of P2P Lending in India

The Indian P2P lending market is valued at approximately ₹1 billion (approx), with about 20 platforms registered as NBFCs under the RBI. These platforms generate revenue through registration fees, processing charges, and repayment fees, positioning themselves as viable alternatives to traditional lending avenues.

Conclusion: A Step Towards a Transparent Future

The RBI’s updated guidelines mark a significant move towards establishing a secure and transparent P2P lending ecosystem. By addressing issues such as credit risk, fund management, and cross-selling, the RBI is setting the stage for sustainable growth in this sector. Although platforms may face initial hurdles, the long-term benefits of increased transparency, reduced risk, and greater trust are expected to strengthen the P2P lending landscape in India.

We're glad you enjoyed this post on "RBI’s New P2P Lending Guidelines". In our newsletter, we delve deeper into these topics and provide actionable tips and strategies to help you achieve your goals in Alternative Asset class.

🚀 Join Our Exclusive WhatsApp Community! 🚀

Love what you’re reading? Want to stay updated with the latest insights, tips, and discussions directly on your phone? 🌟

https://whatsapp.com/channel/0029Vaa6zPX9RZAcjbLfbr08

Stay ahead of the curve and subscribe to our newsletter for the latest insights and solutions!

Still Stuck? Ask Away

Write us at hello@realproft.com with any questions you have about real estate investing. We're here to help you find the perfect way to invest in your future!

Image Sources: Google Images

Email us: hello@realproft.com

Social media

Subscribe to our newsletter to stay up-to-date with all the latest news and updates. By subscribing, you will receive regular emails containing valuable information, exclusive promotions, and exciting announcements. Don't miss out on this opportunity to join our community and be part of the conversation.

Call us: +91 7678255904